Rent the intelligence. Keep your alpha.

Editorial

Welcome back, Embedders. Palantir's Alex Karp gave this week its sharpest line, telling CNBC that enterprises are paying for "tokens that create no value" while handing the labs their alpha (CNBC). He is talking his own book, but the point lands, and it rhymes with older, duller research on who actually beats their cost of capital. AI is compounding faster than anything in history, which is exactly why most companies will lose money on it. The reflex is to spend into the fastest-growing market on earth; the discipline is the opposite, rent the intelligence where it has become a commodity and keep the layer that carries your edge, your data and your workflows, in-house. Below, the case in full, and a week where AI's bill showed up from Washington to your payroll.

- Vas

The research

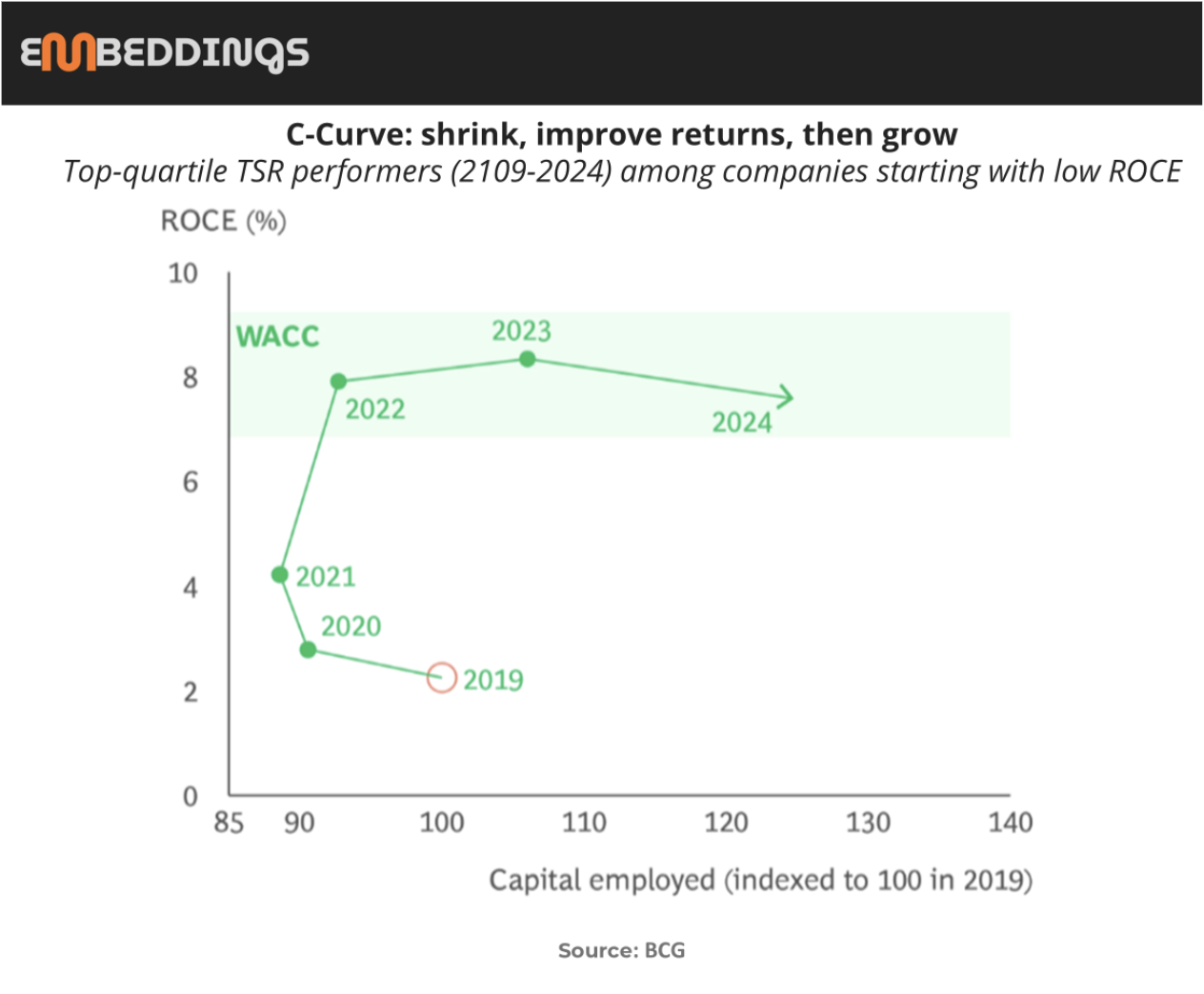

Start with the uncomfortable part. Earning less than your cost of capital is not a rare failure, it is a common condition. BCG's new work on low-return businesses finds that persistently low returns on capital affect about one in seven public companies globally, and whole divisions inside otherwise healthy companies sit there too (BCG, The C-Curve). The instinct is to grow out of it. The data says that rarely works. The companies that escaped did the opposite: they shrank to an advantaged, profitable core, raised returns, and only then grew, delivering 28% total shareholder return over five years while the ones who chased growth first created almost nothing.

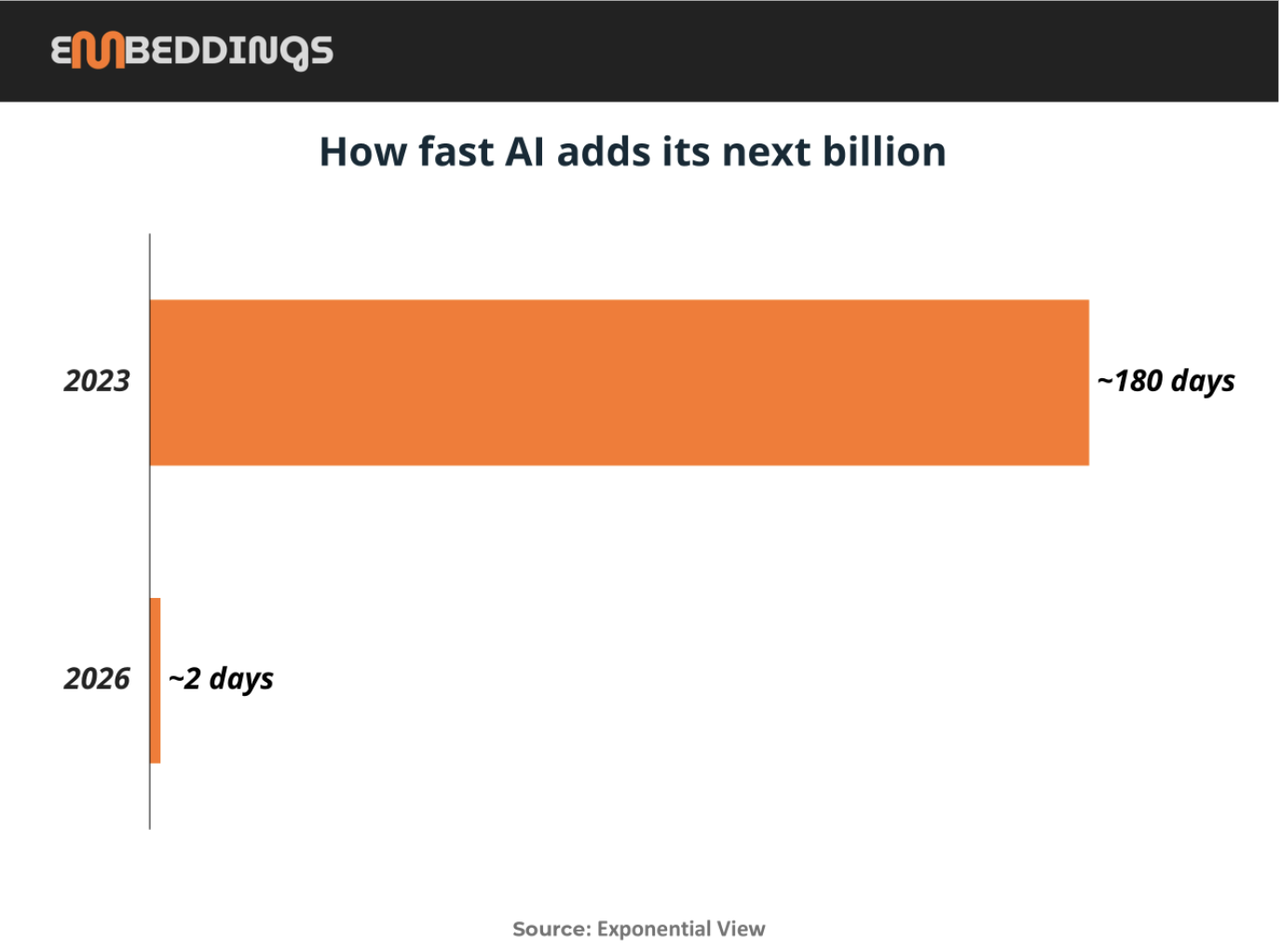

Now set that against the one market compounding fast enough to make discipline sound quaint. At a $175 billion run rate, AI revenue is forming so fast the industry books a fresh billion dollars every two days, against roughly 180 days back in 2023 (Exponential View). Treat the billion-every-two-days line as a speedometer, not proof of profit, it is the run rate restated in a more vivid unit. The substance underneath is what matters: demand is elastic, every 10% drop in token prices tends to lift usage 12 to 18%, so the market grows as it gets cheaper. That is why every board wants to spend into it. It is also exactly where the trap opens.

Days to add the next $1B of AI revenue. Source: Exponential View. The 2026 figure is a run-rate restatement, not audited flow.

Because the default way to buy AI, renting intelligence by the token, is a growth reflex, not a returns one. Palantir's Alex Karp put it in his usual blunt terms this week: enterprises are paying for "tokens that create no value" while handing the labs their data and their edge, their alpha (CNBC). Discount the messenger, he is selling the air-gapped alternative, but the point rhymes with BCG's. You do not out-earn your cost of capital by pouring money into the fastest-growing market on earth and giving away the one asset your valuation has not already priced, your proprietary data and workflows. The disciplined move in the AI economy is the same as it has always been: use AI to raise returns on your advantaged core, and treat your alpha as capital you refuse to spend.

It helps to see the stack. There are three layers: chips at the bottom, models in the middle, applications on top. Nvidia owns the bottom and the middle is a price war, which is why the model layer keeps climbing into the application layer, shipping agents, ad units and enterprise products, and drawing your data and workflows in as it goes. The layer you think you are renting from is trying to become you. Guarding your alpha is how you keep the value where you can bank it. Cheap to rent is not the same as cheap to own.

The alternative is not to stop buying AI. It is to draw the line at your data. A good-enough model is now a cheap, swappable commodity, so treat it like one. The trap is the default way companies buy it: routing your proprietary data and workflows through a lab's metered API, where the lab sees everything and turns it into its own edge. Keep that layer on infrastructure you control instead, open-weight models you run, or rented ones under contracts that forbid training on your data and retain nothing. Use the intelligence, do not feed it your alpha.

The big picture

Washington may become an OpenAI shareholder. OpenAI has reportedly offered the US government a 5% stake, about $42.6 billion, as donated shares rather than a cash sale (FT, via TNW). Read it as insurance, not generosity: equity to cool the temperature ahead of Sanders's plan to tax large AI firms 50%. When you hand the state stock, you expect the heat to rise.

Cybercrime's skill floor just dropped to the price of an agent. Sysdig says it caught the first ransomware attack run end to end by an AI agent, no human at the keyboard: old unpatched flaw, stolen credentials, wiped database, ransom note (TNW). No single move was clever; the model stitched 600 of them together itself. The autonomy that compresses your workflows compresses an attacker's.

Payroll is turning into AI budget. SAP will freeze most hiring, pause non-AI travel and squeeze suppliers to fund a "significant" AI push, its stock down about a third this year (Bloomberg, via TNW). Oracle, Salesforce and Microsoft are doing the same. Incumbents funding AI by cutting themselves is what happens when they believe the threat is real.

Marketing / enterprise

OpenAI's ad business is growing up. Job listings show OpenAI moving past its single text-and-image unit toward image, video, native and conversational ads, with privacy guardrails built into the roles (Digiday). The hard part is the dual-alignment problem: user trust versus advertiser value. Ads inside an advice engine are a different animal from ads beside search.

Marketing Embeddings is read by 20,000+ CMOs, CTOs, and media leaders navigating AI’s impact on marketing. Forward this to someone who needs to see it.